BlockFi is an exchange platform wherein users have plenty of options to deal with cryptocurrency. You can earn from crypto, take loans, and trade with different cryptocurrencies.

BlockFi allows crypto-assets owners to borrow money and it pays interest to cryptocurrency investors. BlockFi aims to provide loans with as low as 4.5% interest, while assets owners can gain interest as high as 7.5%.

It strictly follows the rules and regulations under USA law. BlockFi also enjoys its support from big-names such as CMT Digital, Castle Island Ventures, Morgan Creek Capital, SCB 10X, Avon Ventures, and Purple Arch Ventures. They have got headquarters in Jersey City, New Jersey, USA, and they are located globally across Argentina, United Kingdom, Poland, and the Asia Pacific countries like Singapore.

In the fall of 2017, Zac Prince and Flori Marquez thought of building a company that will provide credits in market service with limited access to savings account. This led to the emergence of BlockFi, which is now a famous cryptocurrency exchanger and secured non-bank lender. In January 2018, it started giving fiat cash against the collateral of cryptocurrency. The platform follows blockchain technology. It provides offers such as lending US dollars for bitcoins and other cryptocurrencies.

How to create an account?

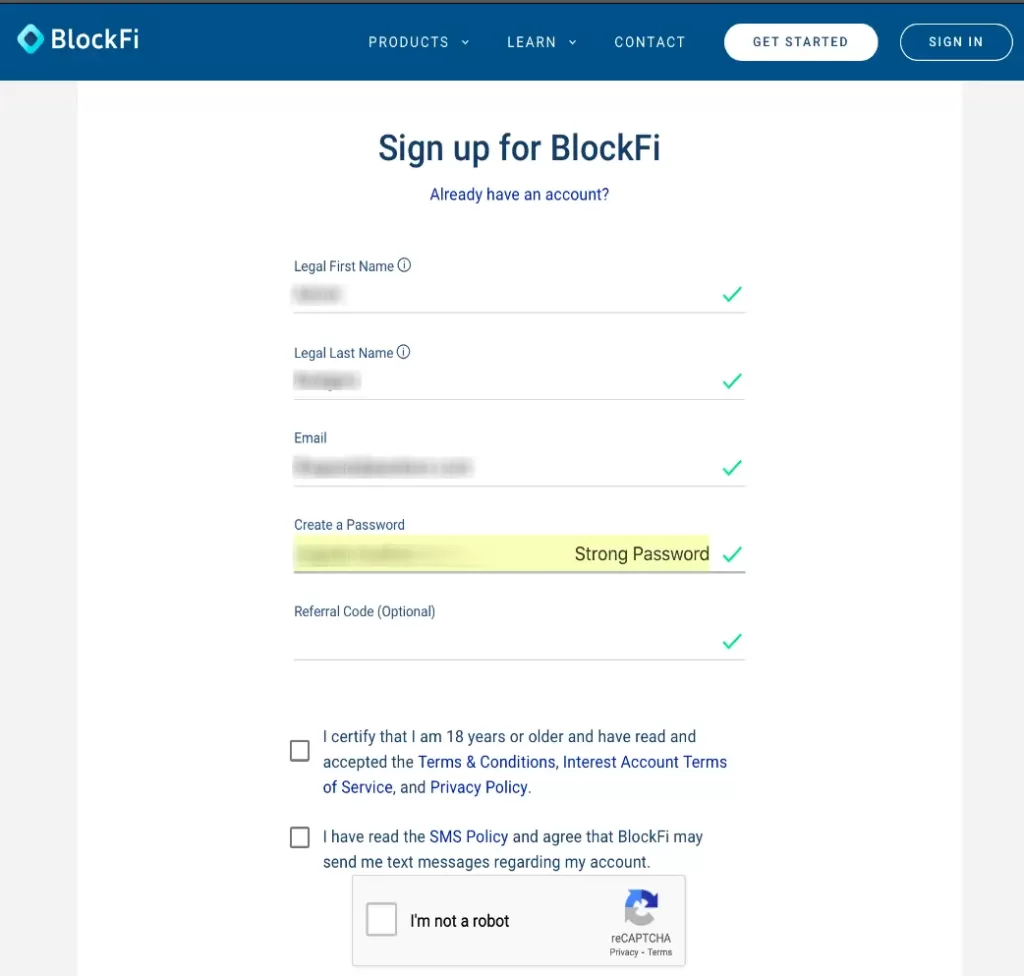

Creating a new user account with BlockFi is a simple process. Firstly, you need to go to BlockFi’s official website to sign up. You’d need a scanned photo and identity documents for the same. Next, you have to check on the terms and conditions, interest account terms of service, and privacy policy. After clicking submit button, a verification email will be sent to your mail address.

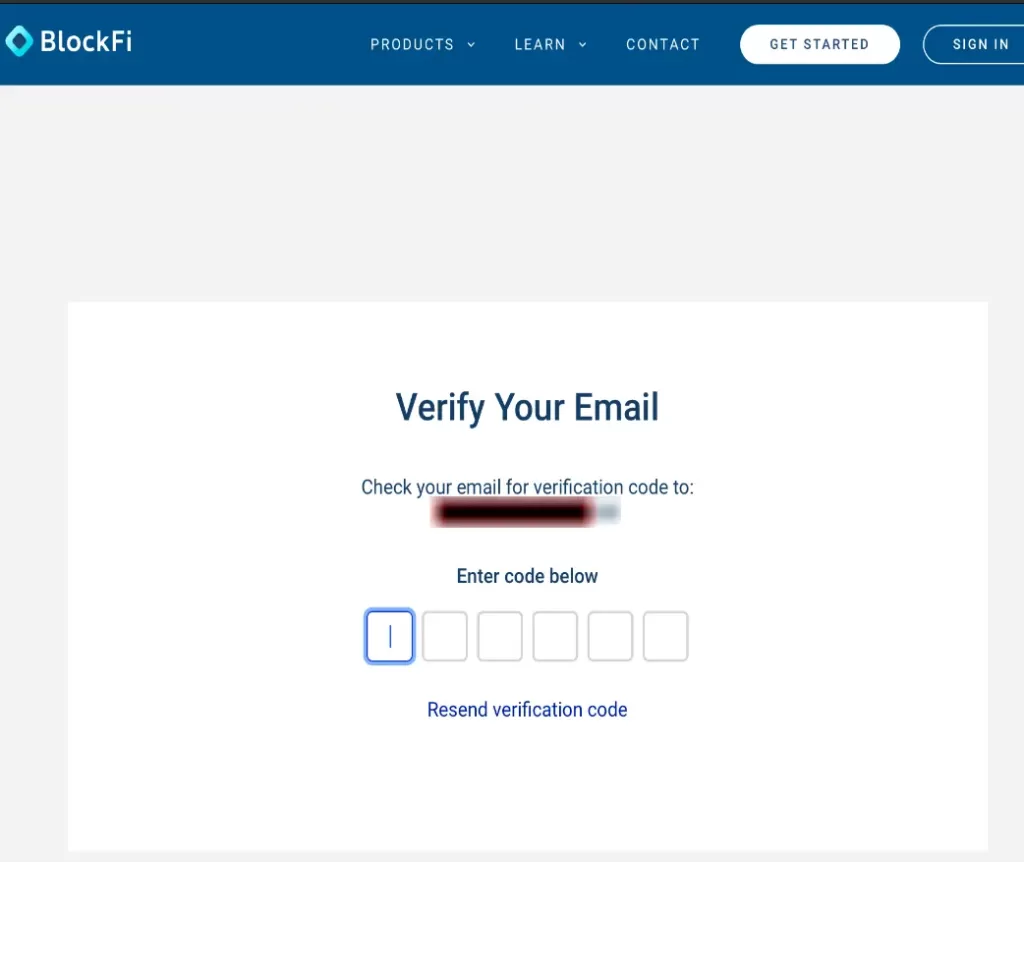

Then you have to check the code in your email and enter it in the required boxes for email verification.

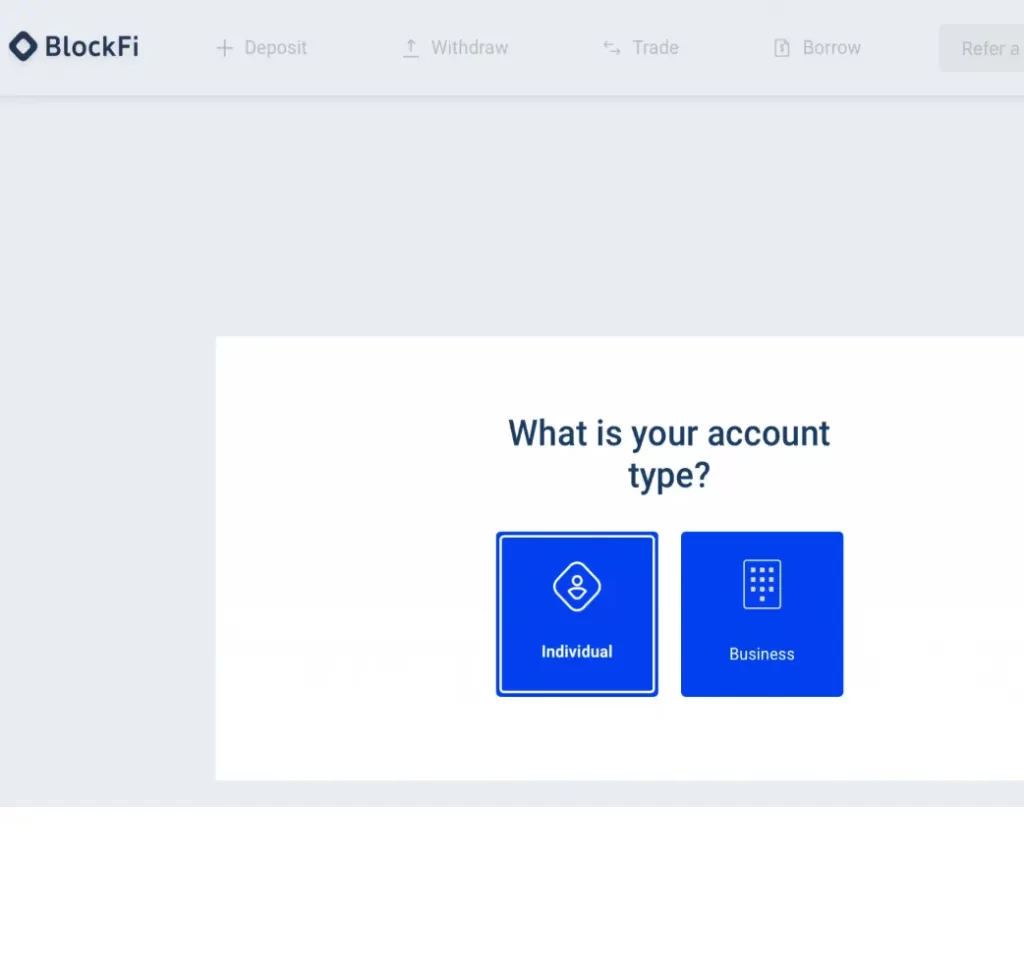

In the next step, you’ll have to choose your account type-Individual or Business

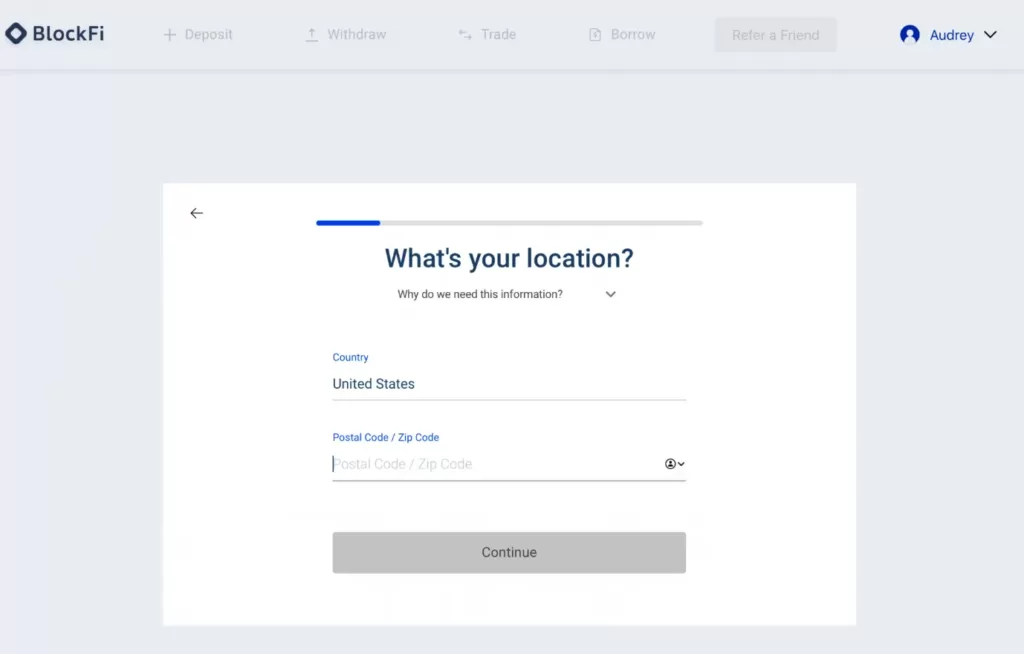

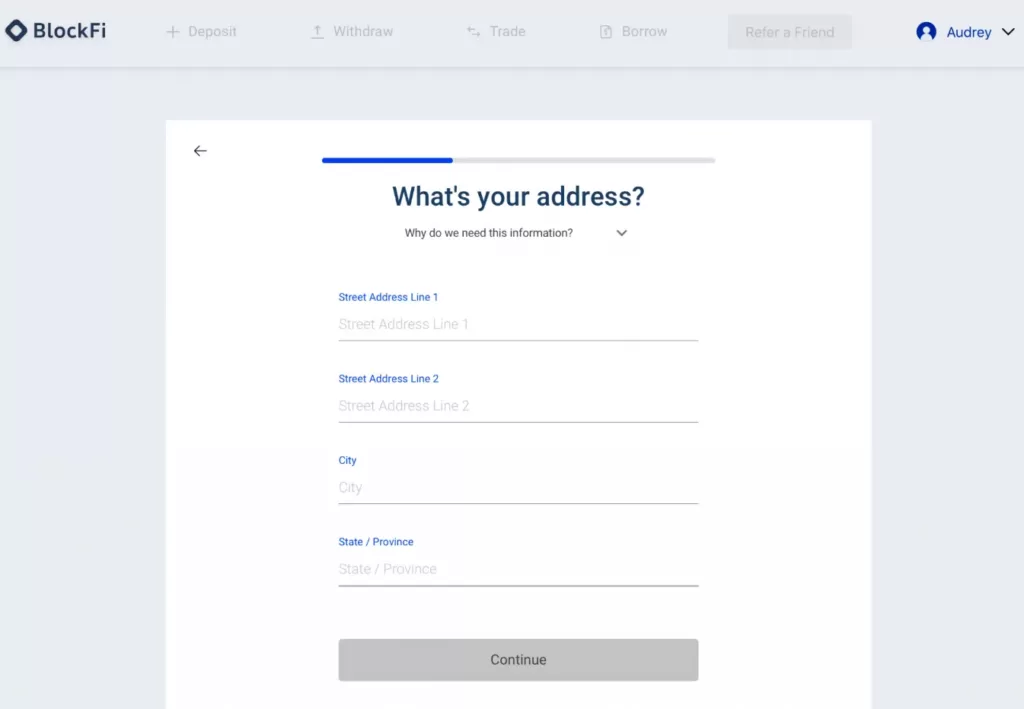

After that, if it’s an individual account, you have to provide a location and address details for security purposes.

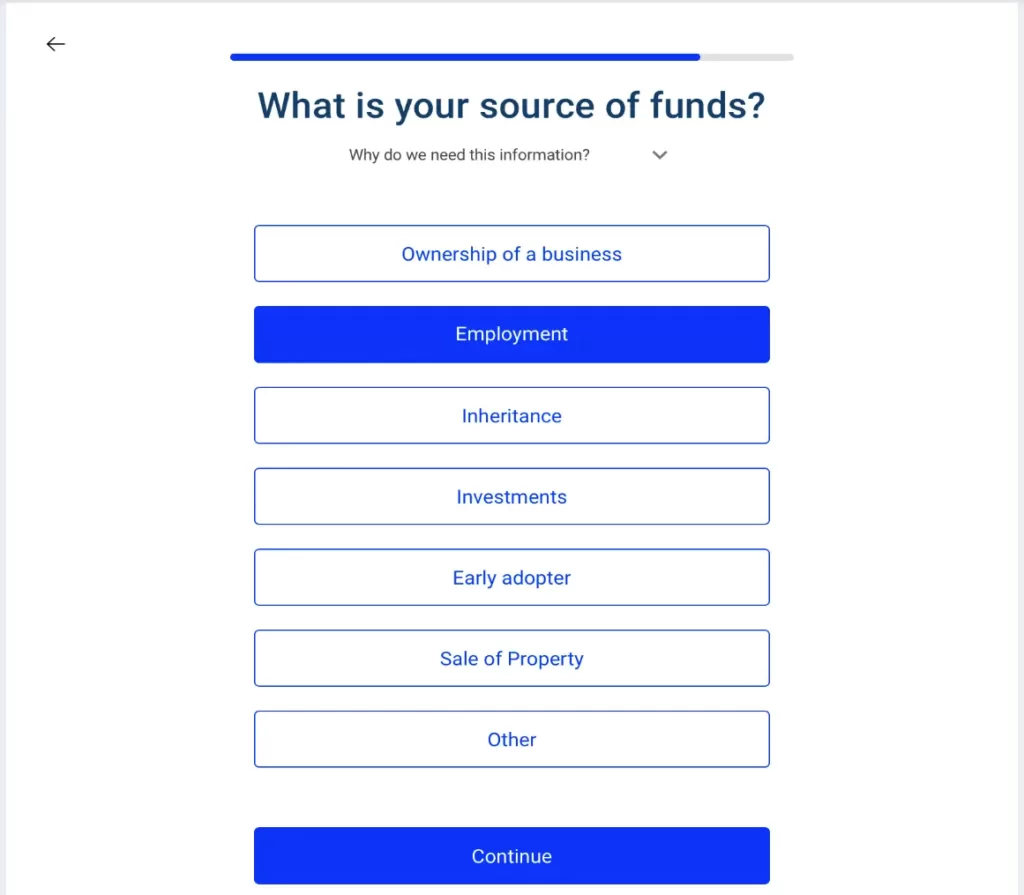

Next, you have to fill in generic blanks such as date of birth and phone number. Then, you have to specify the source of your funds-

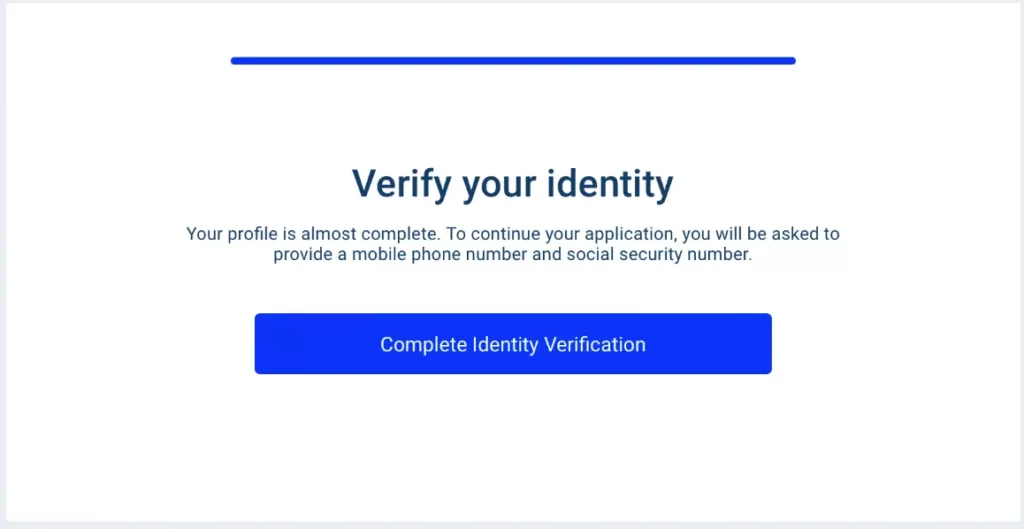

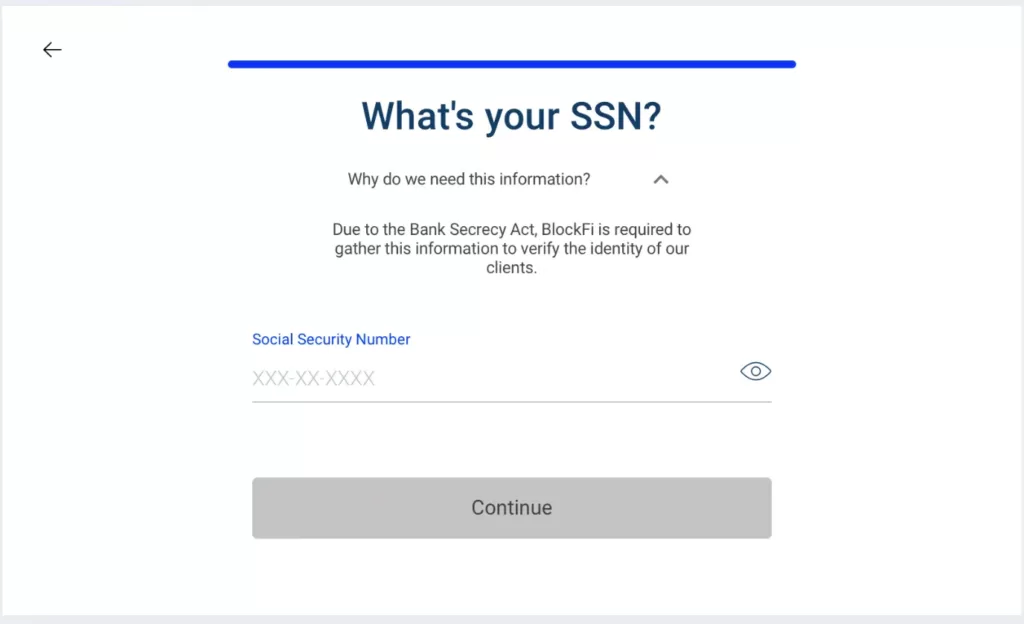

Next is the crucial step about social security questions but before answering them, please verify your identity and provide SSN. One good feature associated with every verification page is the Tab-‘Why this information is needed’. You can go through it to have a decent idea.

Once you have completed all the formalities, BlockFi will open a new account within few minutes. You can then connect your personal bank account, and the transfer of funds will be carried out in ACH.

BlockFi offers only two accounts, personal and business accounts, and no joint account or custody. Moreover, in the case of a Business account, you need to select your business type from Sole proprietors, limited partnership, general partnership, limited liability partnership, limited liability company, corporation, trust account, self-directed IRA.

Security

Security is an integral part of any other crypto exchange due to the risk of hacks as these deal with an enormous amount of money. With BlockFi, one crucial security system is the 2FA, which provides a layer of extra protection to your account. You can do this by Google Authenticator app, which is available on both iOS and Android.

After enabling it, you can access your BlockFi account only through the code generated by the app. As the code is generated every 30 seconds, it’s good to note down the code in a secure place. The other security measures they follow are that most of your funds are stored offline, and the company claims to return your funds safely if the bank faces a crisis.

BlockFi is ready to answer all security questions like KYC, password reset, change of email id, etc. However, they cannot give security like actual banks do or provide insurance as FDIC or SIPC. Yet, they are associated with Gemini Trust company, a licensed depository trust. Hence it offers type 1 security compliant service associated with New York state department financial services.

Though there are reports regarding the hacking of the BlockFi employer account, it is seen that no funds were lost in the process. Hackers tried to access users’ information like date of birth, allocation address, and user activity. However, the security system worked perfectly so the funds could be retrieved within a brief period.

For the ease of its users and to facilitate crypto trading on the move, BlockFi has launched its mobile application for both Android and iOS devices. The app offers functionality such as checking account balance, trading, borrowing, and earning interest on the move. You can install the app from the Apple Store or Play Store, and signing up is easy.

Supported currencies

BlockFi supports eight currencies: BTC, ETH, LTC, LINK, DAI, BAT, UNI, and PAX.

Supported countries

As of 2019, BlockFi is supported in 47 states of the US, and interest accounts are accessible to anyone worldwide except states and countries sanctioned by the US, UK, or EU.

BlockFi Fees

BlockFi believes in the policy of ‘no hidden fees. It charges no trading fees while it charges a small amount for withdrawing currency from your exchange account to your bank account. You are allowed to make one free withdrawal per month, and after that, you will incur a small fee for each withdraw. For example, for BTC- 100 per week @ 0.0025 BTW that comes around $30.

How to withdrawal and deposit money on BlockFi

Withdrawal and deposits are easy with BlockFi. Users can add 500 dollars to the personal account per day, and for a business account, 1000 dollars can be added up per day. Reports say that BlockFi will expand daily limit money in the future. Compared with other traditional investment accounts, BlockFi seems to offer a 43x high-interest savings account.

For making deposits

Open the website home page and click on the deposit option appearing at the top.

A drag-down box of available currency will show up. Choose your preferred currency, such as USD.

Payment methods include transfer via ACH or wire. Next, you have to link your bank account, protected by the notable ‘Plaid.’

Select your bank and enter your credentials, and you will be redirected to access your bank account.

Enter the amount you want to deposit and click on the submit button to finish a transaction. The minimum amount which you can deposit is $20.

For withdrawal of money

There are two ways of withdrawing money: the first one is withdrawing to the bank as USD, and another is withdrawing as Crypto. The Company sets a 1:1 ratio for the bank via ACH or wire in the USD withdrawal process.

Withdrawal via bank transfer is available both in mobile and web versions. First, select the stable coin you want to withdraw from and select ‘Bank transfer(ACH)’ The minimum withdrawal amount is $10.

To protect the clients from fraudulent requests and allow clients to cancel a withdrawal request if they have entered the destination wallet incorrectly, BlockFi places a security hold of one business day. BlockFi also provides time to ensure and review your assets to avoid suspicious or fraudulent activity.

Also, the withdrawal money limit is 5000 dollars per wire withdrawal and you can withdraw money anytime you want. Ideally, it will take one to five business days for the amount to hit your bank account.

Pros and Cons

Here are the pros and cons of the platform:

Pros

U.S.-based and regulated

Instant trades

No commission fee

No monthly fees or minimum deposits

Available worldwide, except sanctioned or watch-listed countries

High yield on your cryptocurrency deposits

Ability to borrow against your crypto assets

No minimums or monthly fees

Cons

No joint or custodial accounts

Limited free withdrawals from interest accounts

APY and loan rate volatility

Savings aren’t protected against bank failure

Not FDIC or SIPC insurance present

Depending on borrower demands, rates can be changed

Limited to one free withdrawal per month

Summary

BlockFi seems to be a very constructive and well-organized cryptocurrency exchange prevailing in today’s market. It is pretty easy to set up and can help you trade popular cryptocurrencies. Cryptocurrency for beginners can be risky and highly speculative, but people can make something huge out of it with the correct approach and suitable exchange services like BlockFi.

One of the most exciting features of BlockFi includes its decent interest rate for traders and its policy of putting customer satisfaction at the top. Though ‘No deposit’ and ‘non-Sipc protected’ funds will face some risks, but with its high-security system and Gemini as custodian, you can be somewhat relaxed with your funds. Another essential factor of this exchange is being regulated by the US, which provides that extra brand value and authority. For all these facts, Block fi is now considered as the future of finance.